Massachusetts (and all states) should end accelerated cost recovery for gas pipeline replacement

Massachusetts legislators are currently debating S.3143, An Act to save people money, repair the climate and grow the economy — a comprehensive energy bill introduced last week. While there is a lot to the 100+ page bill, a key component is a proposal to eliminate the Gas System Enhancement Plan (GSEP) program by 2030. GSEP is the Commonwealth’s accelerated cost recovery mechanism for gas distribution system pipe replacement. The Senate proposal has already drawn pushback from gas utilities and their largest contractor, private-equity-owned Feeney Brothers.1

This post not only applauds the repeal effort but also urges Massachusetts legislators to end the program sooner than 2030.

Legislators and regulators in the District of Columbia and the 42 other states with similar programs should follow Massachusetts’ lead by proposing similar reforms. The main reason is straightforward—in Massachusetts and elsewhere, the primary outcome of these programs is not a safer gas system but a more expensive one.

Utilities and their contractors have made two main arguments in defense of GSEP:2

Safety will be threatened by ‘leaving more dangerous leaks in the ground;’ and

Repealing GSEP will not deliver meaningful ratepayer relief because the program entails only a modest surcharge on customer bills.

Both arguments are wrong. Let’s look at why.

Would ending GSEP make the gas system less safe?

No. Safety obligations don’t depend on how pipeline replacement is financed.

Gas utilities are required by federal and state law to operate safe systems regardless of how pipeline investments are financed.

GSEP is not a “safety” program. It is a financing mechanism that allows utilities to recover capital investments more quickly. Gas utilities like this mechanism because it aligns with their interest in growing utility earnings, creating predictable future cash flows, and sustaining their share prices and credit ratings. Without GSEP, utilities can still undertake replacement projects but they would need to be approved largely through standard rate cases where they receive more comprehensive prudence review and regulatory scrutiny compared to the GSEP review, which is highly time constrained.

Moreover, there is growing evidence that replacement decisions are often poorly aligned with measured risk. In both GSEP and rate case dockets, experts have provided considerable evidence that “there is often little relation between the GSEP risk scoring methodology … and the actual GSEP work that is completed.”3

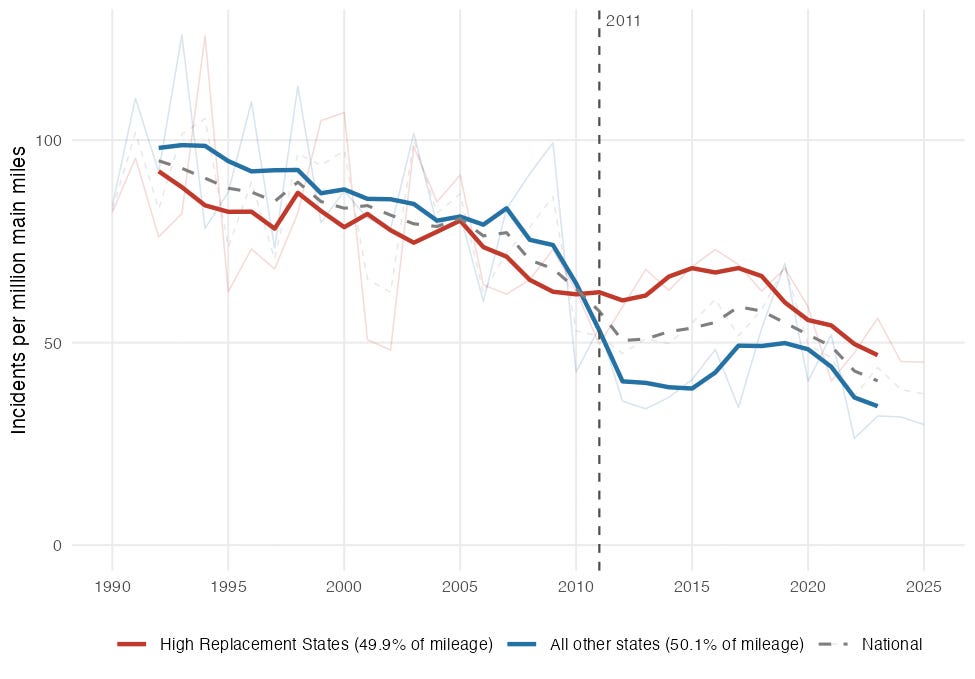

FOHI will release a major study next month that finds that, although pipeline replacement spending rose dramatically after 2011 — when the Pipeline and Hazardous Materials Safety Administration (PHMSA) launched its Call to Action — the increase produced no statistically significant step change in the rate of "significant incidents" reported to PHMSA nationwide. Those incidents have been on a secular decline since the mid-1980s. Even more telling, the dozen states—Massachusetts among them—which replaced the most leak-prone pipe since 2011 have not seen a lower incident rate compared to other states (see Figure 1). From 2011-2018, these high-replacement states actually saw an increase in the rate of significant incidents on their systems. That is the opposite of what one would expect if replacing these pipes reliably reduced risk and improved safety.

Figure 1. Significant Incident rates diverged across states that replaced more or less pipe from 1990-2025

Source: Dorie Seavey, Justin Gundlach & Jack Lewnard et al., Future of Heat Initiative (forthcoming), Spending and Safety Outcomes in U.S. Gas Distribution Systems: An Assessment of DIMP & PHMSA’s Call to Action.

What these data suggest is not just that accelerated replacement did not reduce the rate of significant incidents but also that pipeline replacement activity might itself be a source of risk. These clear empirical findings refute the argument that pipeline replacement is critical for lowering the risk present in gas distribution systems.

But isn’t the GSEP surcharge only a small part of customer gas bills?

Gas utilities in Massachusetts and their large-scale contractors frequently argue that phasing out GSEP will not deliver meaningful ratepayer relief. During Winter 2024-2025, in response to a jump in home heating costs, gas utilities were quick to point a finger at Mass Save, the state’s energy efficiency program because, at the time, the surcharge for it exceeded the GSEP surcharge for many utilities. Utilities proposed to defer Mass Save charges until the off-peak season, arguing that this would reduce gas bills. This reinforced the perception that Mass Save was to blame for the heating bill hikes.

But the argument that GSEP customer charges are somehow de minimis is highly misleading in two key ways:

1. GSEP costs more than just the GSEP surcharge. Each time a gas utility completes a rate case, tens of millions—and sometimes more than a billion dollars—of accumulated GSEP investments are rolled into the utility’s permanent base rates. The GSEP surcharge is then reset to recover only the costs of the newest projects.

National Grid provides a clear example. In its 2020 gas rate case, the company rolled approximately $601 million of investments completed between 2017 and 2019 into its base rates.4 In its current gas rate case, it seeks to roll in another $1.27 billion of GSEP investments made between 2020 and 2024 into base rates.5 Similarly, in November 2025, NSTAR transferred $1.04 billion of capital investments into its base rates, roughly two-thirds of which were attributable to GSEP.6

As a result, the true cost of GSEP on customer bills is largely invisible to customers and policymakers because most GSEP spending has already been embedded in basic delivery rates. A thought experiment drives this home: Suppose the GSEP program ended tomorrow. Most costs would vanish from the surcharge, but customers would keep paying for past GSEP work for decades: the costs already incorporated into base rates stay embedded in the monthly delivery charge—along with the utilities’ return on capital—until they are fully paid off.

2.The GSEP surcharge is also an unreliable measure of what customers actually pay because utilities can reduce or even temporarily eliminate it without reducing GSEP costs. The GSEP surcharge is readily adjustable by utilities in two ways. First, the charge will decrease as previous spending is rolled into base rates (and, conversely, increase with new GSEP spending). For example, the GSEP surcharge for Eversource Gas of Massachusetts declined by two-thirds from November 2024 to November 2025 due at least in part to a GSEP capital roll-in. Secondly, with Department of Public Utilities (DPU) approval, gas companies can temporarily reduce or eliminate the surcharge in order to soften the appearance of rising delivery charges while continuing to recover GSEP through base rates. For example, to voluntarily offset the sharp increase in its base delivery charge following its late 2025 roll-in of prior GSEP spending, NSTAR temporarily reduced its GSEP surcharge to zero.7

GSEP costs have ballooned with little to show for it

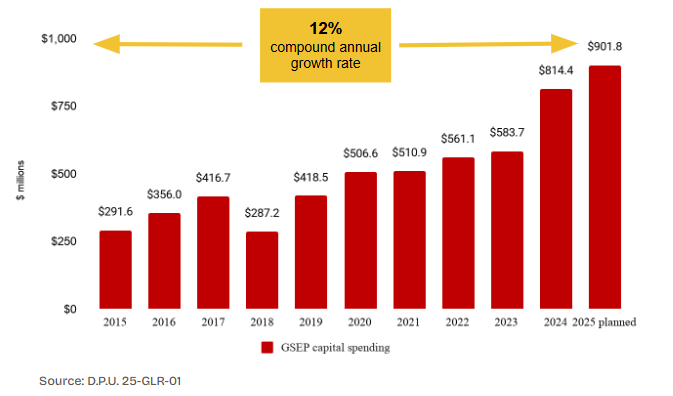

Since GSEP began just over a decade ago, its annual spend has grown at a 12% compound annual rate, exceeding $800 million in 2024, with planned spending of over $900 million in 2025 (Figure 2). During the same period, the combined gas plant of Boston Gas, NSTAR Eversource, and Eversource Gas of Massachusetts increased from $6 billion to $15 billion.

Figure 2: GSEP capital spending ballooned over the last decade

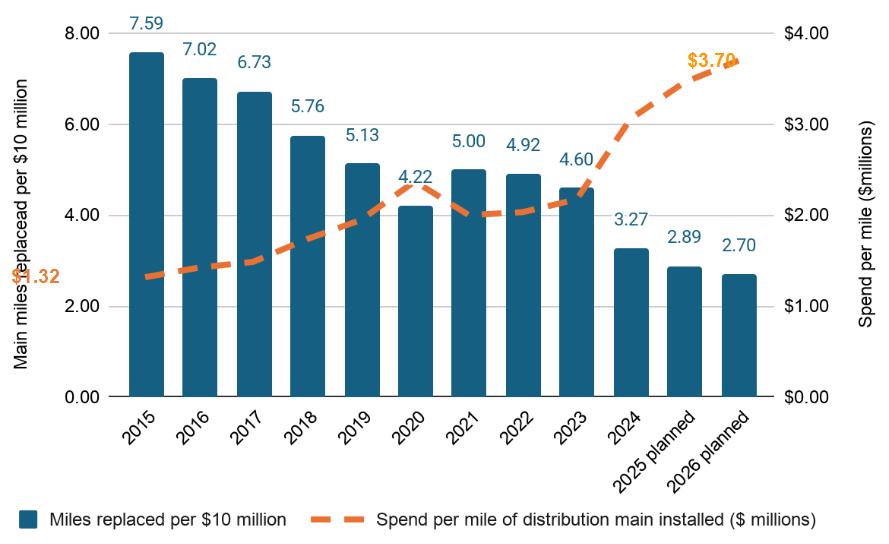

Yet GSEP’s capital productivity has moved in the opposite direction (Figure 3). The cost of replacing a mile of gas main has risen from $1.32 million in 2015 to a projected $3.7 million in 2026—a 180% increase. Put differently, far fewer main miles are being replaced per dollar: a decade ago, utilities replaced 7.6 miles of main for every $10 million; today they replace only about 2.7 miles.

Figure 3: GSEP’s capital productivity has been declining (measured two ways)

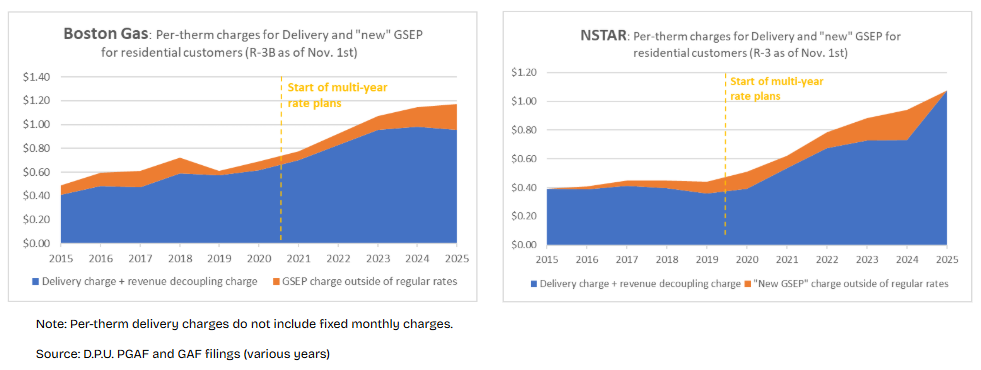

Massachusetts gas customers are paying more while getting less pipeline replaced for every dollar invested, even as GSEP spending, along with other capital spending, has become the primary engine driving up customer bills. Delivery-related charges—which pay for the pipes, not the gas commodity that flows through them—now dominate gas customers’ bills. For the three largest utilities, these charges have been rising 9-10% per year (Figure 4).

Figure 4: Capital spending on the Massachusetts gas system is quietly driving rising customer costs

The end result for Massachusetts gas customers? The typical residential customer used 19% less gas in 2024 than they did in 2014, yet their total bill was up over 50% (Figure 5).

Figure 5: Gas bills in Massachusetts are on the rise even though residential customers are using less gas

Customers may be surprised to learn where those delivery charges go. We estimate that 40% of the average per-therm distribution charge supports recovery of utility capital investments before the separate GSEP surcharge is even added. Of that 40%, about three-fifths goes to utility profits and financing costs associated with the investments while the remaining two-fifths repays pipeline construction costs.

A better path forward: Eliminate accelerated recovery for replacement and focus risk mitigation on measures that deliver the greatest safety benefits for the lowest cost

The DPU itself has already recognized many of the above concerns, determining that pipeline replacement is “the most expensive path for customers and the one most profitable for the LDCs”.8 The Department concluded that “ratepayers simply cannot afford to continue down this path…” and took measures to institute cost containment and improve risk assessment.9

The legislature should build on that foundation.

First, GSEP should sunset as soon as possible. That will begin bending the cost curve for customers by ending an open-ended capital program that lacks “any meaningful incentive for cost containment.”10 We estimate that, under a phase-out scenario, GSEP’s fully loaded cost through the end of the century, inclusive of utility profits and financing costs, drops significantly—on the order of $19 billion (2022$). The near-term impact is also substantial, with about $2.5 billion in savings over the next decade.11

Second, gas utilities must be required to meet higher standards for how they assess, prioritize, and mitigate risk on their gas systems. Risk mitigation should be driven by transparent, evidence-based risk assessments and rigorous benefit-cost analysis—not broad assumptions that entire classes of pipe should be automatically replaced.

Massachusetts can continue to improve gas safety. But doing so will require focusing resources on the measures that produce the greatest reduction in risk for every dollar customers are asked to pay. That focus for the most part has been lacking in the GSEP program since its inception. Eliminating GSEP in favor of greater scrutiny of capital spending in general rate cases will help ensure that gas utilities spend no more than is necessary to keep the distribution system safe.

See, for example, Jamie Perkins, “How to cut energy bills? Mass. Senate, House Disagree,” The New Bedford LIght (May 19, 2026); Feeney Brothers, “Keep GSEP Working: Protecting Public Safety. Modernizing Infrastructure. Supporting Jobs,”

See sources in note 1 and also: MA DPU, D.P.U. 25-GSEP-05 through 06, Joint Reply Brief of Eversource Energy (Apr. 3, 2026); MA D.P.U. 25-GSEP-03, Initial Brief of National Grid (Mar. 20, 2026).

MA DPU, D.P.U. 26-50, Exh. AG-DPL-1 (May 8, 2026), p. 8.

MA DPU, D.P.U. 20-120, Order (Sep. 30, 2021), p. 144.

MA DPU, D.P.U. 26-50, AG-15-2 (Apr. 15, 2026), p. 2.

MA DPU, D.P.U. 26-50, AG-15-2 (Apr. 15, 2026), p. 2.

MA DPU, D.P.U. 25-53, Exh. ES-ANB (June 16, 2025), p. 23.

MA DPU, D.P.U. 24-GSEP-03, Order (Apr. 30, 2025), p. 28.

Ibid, p. 33.

Ibid., p. 31.

Using somewhat different numbers, the Senate conservatively projects $1.46 billion in savings over the first 10 years

|

|

Thank you again Dorie for this excellent analysis. All part of the unending battle to make organizations accountable for their actions, and reveal how they seek both to deceive us and to influence regulators and law makers to act against the public good maximize their shareholder value beyond what is reasonable and equitable for these law makers' constituents.